James O'Shaughnessy Quotations

-

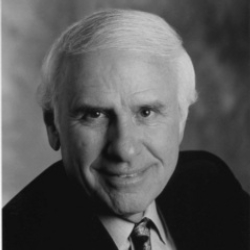

James O'Shaughnessy

Businessman

James Patrick O'Shaughnessyis an American investor and the founder, chairman, and CEO of O'Shaughnessy Asset Management, LLC, an asset management firm headquartered in Stamford, Connecticut... (wikipedia)

James O'Shaughnessy Fans Also Likes Quotations from

Popular tags & topics

-

Art Quotes

Art Quotes

-

Beauty Quotes

Beauty Quotes

-

Friendship Quotes

Friendship Quotes

-

Future Quotes

Future Quotes

-

Happiness Quotes

Happiness Quotes

-

Hope Quotes

Hope Quotes

-

Inspirational Quotes

Inspirational Quotes

-

Leadership Quotes

Leadership Quotes

-

Life Quotes

Life Quotes

-

Love Quotes

Love Quotes

-

Morning Quotes

Morning Quotes

-

Motivational Quotes

Motivational Quotes

-

Positive Quotes

Positive Quotes

-

Romantic Quotes

Romantic Quotes

-

Success Quotes

Success Quotes

-

Time Quotes

Time Quotes

-

Travel Quotes

Travel Quotes

-

Trust Quotes

Trust Quotes

-

Truth Quotes

Truth Quotes

- Explore All Topics...